How to get the most out of compound interest?

We have already seen what the compound interests are and especially the strength of these. For the purpose of this article, I would like to go even further to ensure you have a good understanding of these and allow you to get the most out of them. I would also like to highlight the traps that exist where compound interest might work not for but against you.

As a reminder, compound interest is considered by many to be the eighth wonder of the world because its power is so impressive. In this article, we are going to dive deeper into the world of compound interest.

Reminder on compound interest

Simply put, compound interest is a financial concept that refers to earning interest on interest. For example, putting money into an account where you receive interest based on the amount in that account. After a year, you have received interest in this account and you leave it there. The year after, you will receive not only the interest on the amount initially deposited but on the amount deposited plus the interest previously generated.

Well, the best way to understand this concept is the image of a snowball pushed from the top of a snow-capped mountain. The more it goes down, the more it grabs the snow and gets bigger and bigger. With compound interest, your bank account could act just like this snowball!

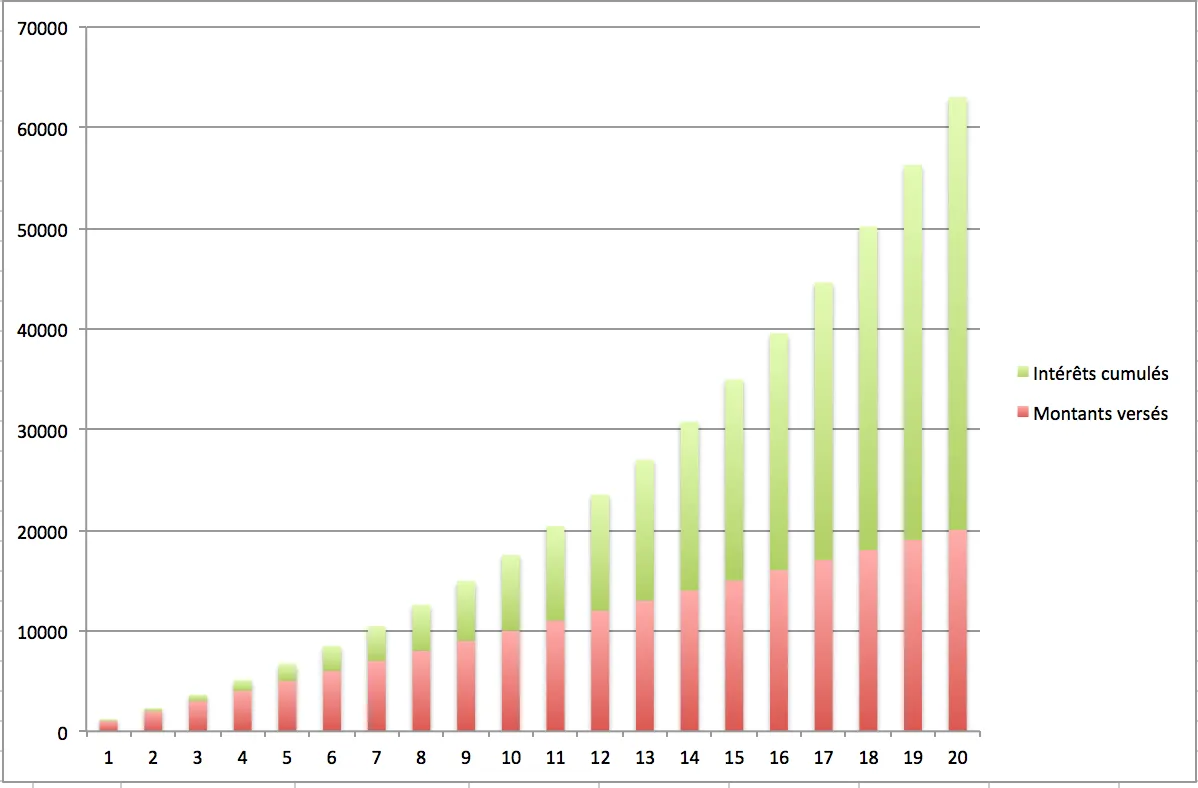

If you want to have a concrete and quantified example of the difference between an investment based on simple interest and on compound interest, I suggest you to read our introductory article on compound interest. But to summarize the results of a comparison, I put below the graph showing the possible evolution of income thanks to compound interest (Annual investment of 1,000 euros at 10%). Please note that the red part illustrates the invested amounts while the green represents the interest.

Compound interest formula

Rule of 72

A formula widely used in the field of compound interest is that of 72. Did you know that this formula allows you to know when you will have doubled your money thanks to the compound interest? To do this, just divide 72 by your interest rate. It’s a very simple but terribly efficient calculation.

As an example, let’s imagine that you could have an interest rate of 8% on a savings account. You just need to divide 72 by 8 to have the time you need to double your investment. In our case, 72/8 = 9. So you would only need 9 years to double any investment made in this platform.

Complete calculation

This rule of 72 is not bad and allows you to get a quick idea of the capabilities of compound interest. But, if we want to go further in the analysis it is important to know how to calculate the end result of an investment benefiting from compound interest.

To establish this formula, we need to establish the variables that we are going to use:

- In = Investment after n periods

- I0 = Initial investment

- i = Interest rate for a period

- n = duration of the investment

The formula to use is:

In = I0*(1+i)^n

Take the situation previously analyzed of 8% interest per year where we would invest 10,000 dollars for a period of 5 years.

The result is therefore:

In = 10.000 * (1+0,08)^5 = 14.693 USD

So this formula assumes that interest is paid annually. But let’s imagine that the reality here is that interest is paid every day. We must therefore divide the 8% interest over the 365 days that make up a year and carry out the calculation over 365 days over 5 years and therefore 1,825 periods.

The real result therefore becomes:

In = 10.000* (1+0,00021918)^1.825 = 14.917 USD

This calculation demonstrates the power of compound interest. We see in the above calculation that in the same situation if the interest was paid daily, it would save almost 200 dollars more. This is logical because since we receive interest more quickly, the capital used as the basis for the calculation grows faster.

Examples of compound interest

Examples of positive compound interest

Investments

Take the example of peer-to-peer lending investments and therefore personal loans, for example through the Mintos platform. The platform ensures that once interest and/or principal repayment are received, these funds are invested directly in new loans. Thus, as soon as you receive your interests, they are directly reinvested and therefore increase the capital generating interest.

Thus, as soon as you have funds that you are ready to invest, the platform will be ready to invest them directly and thus set up this compound interest mechanism as soon as you place them.

Either way, as with any investment, but even more so in the case of compound interest, the sooner you start investing the better. The machine must be started as soon as possible.

Savings accounts

This example may seem a little more surprising, especially when you realize how little interest this type of account generates. However, it is indeed compound interest, like the investment developed previously, but with much lower interest.

In fact, your savings account generates interest every year. This interest is paid on the same account where your capital is located. So these interests increase your capital and therefore your basis for calculating interest.

The problem with these savings accounts is that the interest rates offered by them do not beat inflation. We are talking about inflation per year ranging from 1 to 2% in France or Belgium. The savings accounts only allow you to earn interest of 0.01% or even 0.11% if you include the loyalty bonus.

The calculation is therefore quickly done, by leaving our money in a savings account we lose money. Because the 100 dollars that you would have possibly placed in the savings account is actually worth only 99 dollars the year after (considering an inflation of 1%). Thus, it is crucial to put your money in investments that, at the very least, beat inflation.

Dividends

As you probably know, many stocks pay a dividend to their investors. A common practice in the investment world is to directly reinvest dividends received by purchasing new shares of the shares that generated this income. Thus, you hold more dividend distributing shares and therefore, with the next payment, you will get more dividends. So it is indeed the effect of compound interest that operates here.

Note that some stock exchange platforms allow the automatic reinvestment of dividends in shares to be activated directly. This option allows you to not have to worry about it and that everything is managed without your intervention and therefore also without risk of forgetting.

This phenomenon can also be found in mutual funds. These often offer the option “distribution” or “capitalization”. This second option allows the dividends that would have been received to be directly reinvested to acquire more units of said mutual fund.

Note that some stock exchange platforms allow the option of reinvesting dividends in shares of shares directly and automatically. This option allows you to not have to worry about it and that everything is managed without your intervention and therefore also without risk of forgetting.

Examples of negative compound interest

Clearly, we often talk about the benefits of compound interest and what it can do for us. But we often forget that this compound interest can also work for other people and therefore against us. Let’s take a look at some examples.

Credit cards

Credit cards are a prime example of the negative effect compound interest can have when used against us. When you have a standard credit card, you have the flexibility to spend money that you don’t have. So you have a credit balance that increases with your spending. So you’re going to have to pay interest on that balance the bank loaned you. This allows you to keep this credit with regular payment of a proportion of the amount.

But, and this is the trick, the interest you have to pay on that credit balance also comes on top of that balance. Thus, if you do not make regular payments, the balance on which the interest rate is applied will therefore increase by the interest you owe.

That’s why I’m going to recommend anyone not to get into this kind of credit system. It is crucial for your finances to repay the credit amount on your card as soon as possible.

Fees on investments

Another point of care to prevent compound interest from working against you is to be careful with investment fees. Mutual funds and ETFs generate fees for your investments. This is because you have to pay the manager of the fund or ETF a percentage of the amount you invested as management fees. As a reminder, in the case of mutual funds, we usually talk about fees of around 2% while ETFs these fees are of the order of 0.1%.

However, whether in a fund or in an ETF, the more your invested capital increases, the higher your fees will be. So, if we take the idea of capitalization mentioned in the point “Dividends”, your reinvested generated profits increase your interest-generating capital but also increase the capital at the same time as the basis for calculating costs.

I assure you, the gains generated by compound interest far exceed the costs incurred (especially in the case of ETFs). So it is still a good trade if you invest in solid ETFs. But it also demonstrates the value in seeking lower costs and not just increased earnings. Especially knowing that ETFs allow these two gains compared to mutual funds.

Conclusion

The most important thing when talking about compound interest is to start as early as possible. Even if it’s a small amount of money, although it’s not as consistent as it should be. The key is to start. The real power of compound interest is that no matter how small those investments are, maintaining this habit can have a significant impact in the long run. Compound interest rewards people who manage to establish a savings habit and continue to add funds, no matter how small.

Sources

- https://www.abcbourse.com/apprendre/12_lecon_af_10_partie2.html

- https://dollarsprout.com/compound-interest/

- https://france-inflation.com/index.php#:~:text=Sur%20l’ann%C3%A9e%20compl%C3%A8te%2C%20l,avaient%20pronostiqu%C3%A9%20les%20sp%C3%A9cialistes%20financiers.&text=La%20tendance%20court%20terme%20semble,voir%20l’inflation%20remonter%20sensiblement.

- https://www.inflation.eu/fr/taux-de-inflation/belgique/inflation-historique/ipc-inflation-belgique.aspx

- https://www.belfius.be/retail/fr/produits/epargner-investir/epargne/index.aspx

How to grow your passive income with Cross Chain Capital (CCC) - Invest and Me

5 December 2021 @ 7:32 PM

[…] case, we understand that all this will allow the project to grow by taking full advantage of the compound interest. When we talk about investing in other protocols, we could talk for example about the Wonderland […]